All Categories

Featured

Table of Contents

Eliminating agent payment on indexed annuities permits for significantly greater detailed and real cap rates (though still substantially less than the cap rates for IUL policies), and no doubt a no-commission IUL policy would certainly press detailed and actual cap rates higher too. As an aside, it is still feasible to have an agreement that is extremely abundant in representative compensation have high early cash surrender worths.

I will certainly yield that it is at the very least theoretically POSSIBLE that there is an IUL plan out there provided 15 or twenty years ago that has actually provided returns that transcend to WL or UL returns (a lot more on this listed below), however it's crucial to much better recognize what an appropriate contrast would certainly require.

These plans normally have one lever that can be established at the firm's discernment annually either there is a cap price that specifies the optimum attributing rate because certain year or there is an engagement price that defines what percentage of any type of positive gain in the index will be passed along to the plan because particular year.

And while I generally concur with that characterization based on the mechanics of the policy, where I disagree with IUL advocates is when they identify IUL as having premium returns to WL - national life group indexed universal life. Lots of IUL supporters take it an action better and indicate "historic" information that appears to support their insurance claims

First, there are IUL plans around that carry even more threat, and based upon risk/reward concepts, those plans should have greater anticipated and real returns. (Whether they in fact do is an issue for significant discussion however companies are using this method to help justify greater detailed returns.) Some IUL policies "double down" on the hedging approach and assess an additional cost on the plan each year; this fee is after that used to raise the alternatives budget plan; and after that in a year when there is a positive market return, the returns are amplified.

Problems With Universal Life Insurance

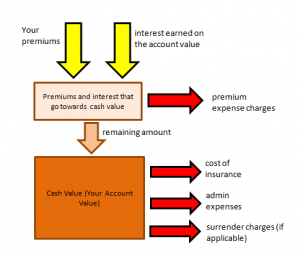

Consider this: It is feasible (and as a matter of fact likely) for an IUL plan that standards an attributed rate of say 6% over its initial one decade to still have a general negative price of return during that time as a result of high costs. So several times, I discover that agents or customers that extol the efficiency of their IUL plans are confusing the credited rate of return with a return that properly reflects every one of the policy bills too.

Next we have Manny's concern. He claims, "My buddy has been pushing me to buy index life insurance policy and to join her company. It looks like an online marketing. Is this a good idea? Do they truly make how much they claim they make?" Allow me begin at the end of the concern.

Insurance coverage salespersons are tolerable people. I'm not suggesting that you 'd dislike yourself if you claimed that. I claimed I utilized to do it, right? That's how I have some insight. I made use of to market insurance coverage at the beginning of my profession. When they market a premium, it's not unusual for the insurance coverage firm to pay them 50%, 80%, also often as high as 100% of your first-year costs.

It's hard to market since you got ta always be looking for the following sale and going to locate the next person. It's going to be difficult to discover a lot of satisfaction in that.

Allow's speak about equity index annuities. These points are popular whenever the markets remain in a volatile period. Below's the catch on these points. There's, first, they can control your actions. You'll have surrender durations, normally 7, 10 years, perhaps even beyond that. If you can't obtain access to your cash, I understand they'll tell you you can take a little percent.

Side Fund Life Insurance

Their abandonment periods are substantial. That's exactly how they understand they can take your cash and go fully invested, and it will certainly be okay due to the fact that you can not get back to your cash till, once you're right into 7, ten years in the future. That's a lengthy term. No matter what volatility is taking place, they're most likely going to be fine from an efficiency point ofview.

There is no one-size-fits-all when it comes to life insurance coverage./ wp-end-tag > In your hectic life, monetary self-reliance can seem like a difficult objective.

Less employers are supplying typical pension plans and several firms have actually reduced or terminated their retired life strategies and your ability to rely entirely on social safety is in question. Even if advantages haven't been decreased by the time you retire, social protection alone was never ever intended to be sufficient to pay for the way of life you desire and are worthy of.

Best Performing Iul

/ wp-end-tag > As component of an audio monetary technique, an indexed global life insurance coverage policy can assist

you take on whatever the future brings. Prior to committing to indexed global life insurance policy, right here are some pros and disadvantages to think about. If you pick an excellent indexed global life insurance policy plan, you might see your money worth grow in worth.

If you can access it beforehand, it might be advantageous to factor it right into your. Since indexed universal life insurance coverage requires a specific level of threat, insurance provider often tend to keep 6. This sort of strategy also uses. It is still guaranteed, and you can adjust the face quantity and motorcyclists over time7.

If the picked index doesn't do well, your cash worth's growth will certainly be affected. Normally, the insurance provider has a beneficial interest in executing better than the index11. There is usually a guaranteed minimum passion price, so your plan's development won't fall below a particular percentage12. These are all elements to be taken into consideration when choosing the most effective sort of life insurance policy for you.

Nonetheless, considering that this type of policy is more complicated and has a financial investment part, it can usually include higher costs than various other policies like entire life or term life insurance coverage. If you do not believe indexed universal life insurance policy is best for you, right here are some choices to consider: Term life insurance coverage is a momentary policy that commonly provides coverage for 10 to three decades.

What Is Universal Life Insurance With Living Benefits

Indexed global life insurance policy is a type of policy that provides extra control and adaptability, along with greater cash money worth growth capacity. While we do not use indexed global life insurance, we can provide you with even more details concerning entire and term life insurance policy policies. We suggest discovering all your alternatives and chatting with an Aflac agent to discover the most effective suitable for you and your family.

The rest is added to the cash money worth of the plan after charges are deducted. While IUL insurance policy may show useful to some, it's crucial to understand just how it works before acquiring a plan.

{kind=link}

Table of Contents

Latest Posts

Difference Between Whole Life And Iul

Index Insurance

Minnesota Life Iul

More

Latest Posts

Difference Between Whole Life And Iul

Index Insurance

Minnesota Life Iul